Q2 2026 New Car Insights

Read what we learned during Q2 below:

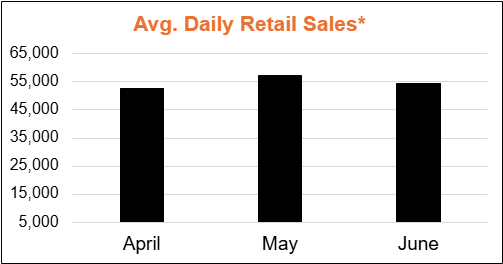

1) 3-Month Sales Trend (Avg. Daily Retail Sales)

Insight: Retail sales increased from April (52,508) to May (57,342) before easing slightly in June (54,552). Despite the June pullback, sales remained above April levels, indicating steady consumer demand through the quarter.

Action:

Stay focused on inventory turn and stocking vehicles that align with local demand. Dealers who actively manage aging inventory and quickly adjust pricing are best positioned to capitalize on consistent retail activity.

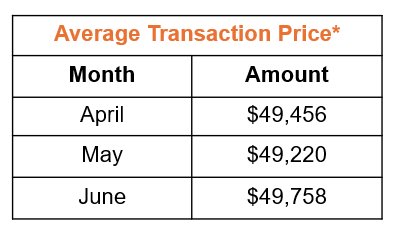

2) Average Transaction Price (ATP)

Insight: Transaction prices remained relatively stable throughout the quarter, ending June at $49,758, the highest point of Q2. The modest increase suggests shoppers continue to purchase higher-priced vehicles despite affordability pressures.

Action:

Maintain pricing discipline and focus on value-based merchandising. Highlight vehicle features, packages, and payment options that help justify higher transaction prices without relying on broad discounting.

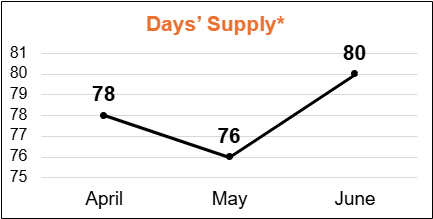

3) Days’ Supply

Insight: New-vehicle days’ supply fell slightly in May before rising to 80 days in June. Inventory levels remain healthy, but the increase suggests supply is growing faster than sales in some segments.

Action:

Monitor aging inventory closely and adjust pricing strategies before vehicles become over-aged. Use market-based inventory management to ensure supply remains aligned with demand.

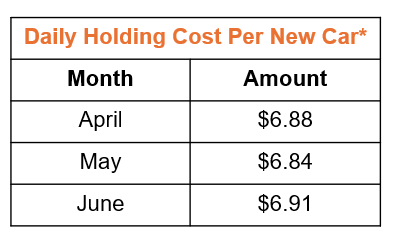

4) Daily Holding Cost per New Car

Insight: Holding costs remained essentially unchanged throughout the quarter, ranging from $6.84 to $6.91 per vehicle per day. While costs remain stable, increasing days’ supply can compound overall carrying expenses.

Action:

Reduce time-to-sale by prioritizing fast-turn inventory and ensuring vehicles are frontline-ready quickly. Faster inventory movement continues to be one of the most effective ways to control holding costs.

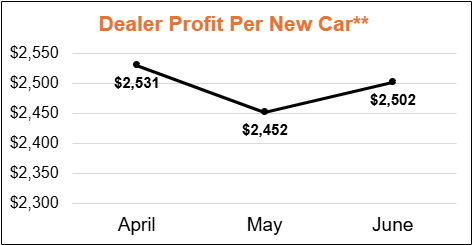

5) Dealer Profit per New Car

Insight: Profit per new vehicle declined in May before recovering in June to $2,502. Profitability remained relatively consistent despite fluctuations in sales volume and inventory levels.

Action:

Protect gross on high-demand vehicles while using targeted incentives to move slower-turning inventory. Focus on inventory mix and pricing strategy rather than blanket discounting.

Q2 2026 Used Car Insights

Read what we learned during Q2 below:

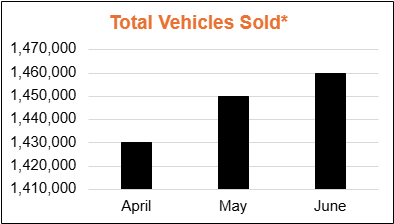

1) Total Vehicles Sold

Insight: Used-vehicle sales increased each month during Q2, rising from 1.43 million units in April to 1.46 million units in June. Consistent growth signals continued consumer demand in the used-vehicle market.

Action:

Maintain a steady acquisition strategy and avoid inventory shortages. Consistent sourcing and disciplined inventory management will help dealers capitalize on sustained demand.

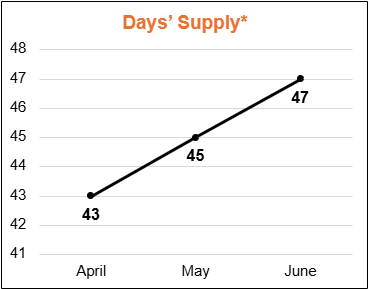

2) Days’ Supply

Insight: Used-vehicle days’ supply increased from 43 days in April to 47 days in June. While inventory availability improved, the increase suggests inventory is accumulating faster than sales in some markets

Action:

Monitor market days’ supply and pricing competitiveness frequently. Take proactive action on aging vehicles before they lose visibility and profitability.

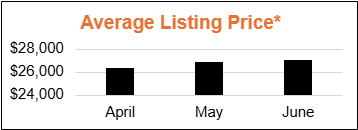

3) Average Listing Price

Insight: Used-vehicle prices rose throughout the quarter, climbing from $26,329 in April to $27,027 in June. The increase reflects continued strength in used-vehicle demand and pricing.

Action:

Review pricing regularly against current market conditions. Rising prices can support profitability, but dealers should remain attentive to affordability concerns that may impact shopper demand.

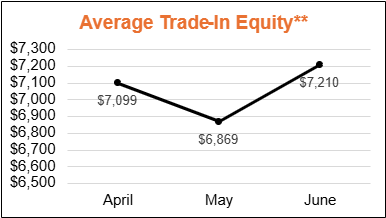

4) Average Trade-In Equity

Insight: Trade-in equity declined in May before rebounding sharply in June to $7,210, the highest level of the quarter. Strong equity positions continue to provide consumers with opportunities to trade into newer vehicles.

Action:

Increase focus on trade-in acquisition opportunities. Customers with positive equity represent a valuable source of inventory and can help drive both vehicle acquisitions and retail sales.

Sources:

* Cox Automotive Insights

** J.D. Power

Q2 2026 Dealer Insights: Inventory, Pricing & Profitability Trends | vAuto Quick Takes

vAuto’s Bethany Johnson breaks down Q2 2026 dealer trends: rising market day supply, near-record new car pricing, negative equity shifts, and profit per unit.

Need to catch up? View our archived insights here.

Interested in a Demo?

Fill out this form to request a personalized demo of any or our solutions.

"*" indicates required fields